The much awaited and biggest regulatory reform in the Real Estate Market of Bengal i.e. #WBHIRA(WestBengal HousingIndustry Regulation) Act, is knocking at the door and will be fully established in the state by the year end. Seminars, educational and awareness initiatives are being implemented state-wise currently so that the industry gets a knack of the upcoming reforms and do not get puzzled all of a sudden. The #WestBengalLegalDepartment has published the revised version of # ...See more

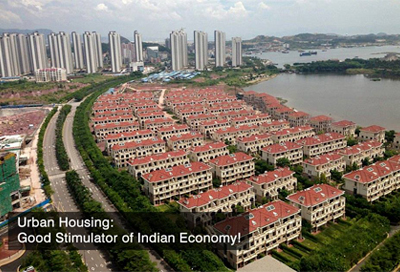

The economics of #urbanhousing is equally important and mutually reinforcing. Due to value addition and monetisation of land, #Urbanhousing has unfurled immense potential to absorb investments and stimulate Indian economy. In the next 10 years, the Indian economy is going to move towards a six trillion dollar #GDP and also will be the largest size of #middleincomegroup across the globe.

Despite a... See more

#OrientalPalms: Own a #home that towers everything else around you and gives you a #smarter life! An executive #clubhouse to also nurture your lavish trimmings. http://bit.ly/2z79Fhm

Lorem Ipsum is simply dummy text of the printing and typesetting industry. Lorem Ipsum has been the industry's standard dummy text ever since the 1500s, when an unknown printer took a galley of type and scrambled it to make a type specimen book. It has survived not only five centuries, but also the leap into electronic typesetting, remaining essentially unchanged.

Contrary to popular belief, Lorem Ipsum is not simply random text. It has roots in a piece of classical Latin literature from 45 BC, making it over 2000 years old. Richard McClintock, a Latin professor at Hampden-Sydney College in Virginia, looked up one of the more obscure Latin words, consectetur, from a Lorem Ipsum passage, and going through the cites of the word in classical literature, discovered the undoubtable source. Lorem Ipsum comes from sections 1.10.32 and 1.10.33 of "de Finibus Bonorum et Malorum" (The Extremes of Good and Evil) by Cicero, written in 45 BC. This book is a treatise on the theory of ethics, very popular during the Renaissance.

A deed of exchange can be signed by property owners once they make up their minds to transfer rights to their properties to one another, in the process, becoming the owner of the other person’s property...

Vastu Shastra is an ancient science that helps us iron out the creases in our lives and keeps evil forces and negative energy at bay. Since proper vastu can create a safe and protective environment for us...

When the ownership rights and responsibilities of a property are collectively held by two or more individuals by a legal arrangement, it is called joint ownership. In this arrangement, each co-owner holds...

Kolkata, which has been terribly supersaturated in the heart of the city for a long time now...

Land is always a critical asset but how does one put a price tag to a parcel of land...

Consumer Buying Preferences at New Town Rajarhat Kolkata...

Kolkata, traditionally an end-user driven market has exhibited vibrant growth in residential real estate market in the past few years.The core city grows....

Eastern Metropolitan Bypass or EM Bypass can be reckoned as one of the major lifelines of Kolkata which has moved much ahead of the curve...

The importance of agents or consultants in an organized real estate market is pivotal.The consultants act as a compact bridge between the buyers and sellers help...

.png)

Contact Us

Contact Us Get Direction

Get Direction